Inverse lognormal distribution

This tool calculates the Inverse of lognormal Cumulative Distribution Function.

Inverse lognormal distribution formulas

X : a random variable following a lognormal distribution

`mu` : location parameter

`sigma` : scale parameter ( > 0)

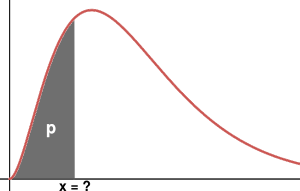

The inverse of the cumulative distribution function F(x) is also called the 'quantile function', denoted Q(x). We have,

`F(x) = 1/2*(1+\text{erf}((ln(x)-mu)/(sigma*sqrt(2))))` pour `x > 0`

which inverse function is,

`Q(x) = exp(mu+sqrt(2*sigma^2)*\text{erf}^(-1)(2*x-1))`

where erf is the Error function,

`\text{erf}(x) = 2/sqrt(pi)*\int_0^x e^(-t^2)\ dt`

See also

Inverse Lognormal distribution

Lognormal distribution Chart

Statistics Calculators